- Published on 10 March 2026

Contents

Introduction

1. Tax Exemption Ceiling Too High

2. One-third of properties are subject to tax

3. Improving Collection Efficiency

4. Improving Assessment Transparency

5. Aspects Skipped by Amendments: Regulating Real Estate Market and Rents

References and Notes

Introduction

On March 1st, 2026, the Egyptian House of Representatives approved amendments to the Real Estate Tax Law.1 Most notably the amendments include an increase of the tax exemption limit on private homes from an annual rental value of LE 24,000 to LE 100,000. Another notable amendment is the provision of incentives for tax payers who have not been exempt, such as a 25% discount on the tax value when paid on time.

The government’s capacity to impose and collect taxes efficiently is linked to the extent of general satisfaction with public service funded by taxes, and to the fair and equitable application of tax collection. Concurrently, to protect the right to housing, Real Estate Taxes could be a tool to regulate the real estate market, whether sale or rent, especially at a time of widespread public outcry over soaring prices. With the House of Representatives passing the amended law, the Built Environment Observatory offers a commentary on the most important amendments, as well as proposals for broader Real Estate Tax reform not addressed by the amendments.

1. Tax Exemption Ceiling Too High

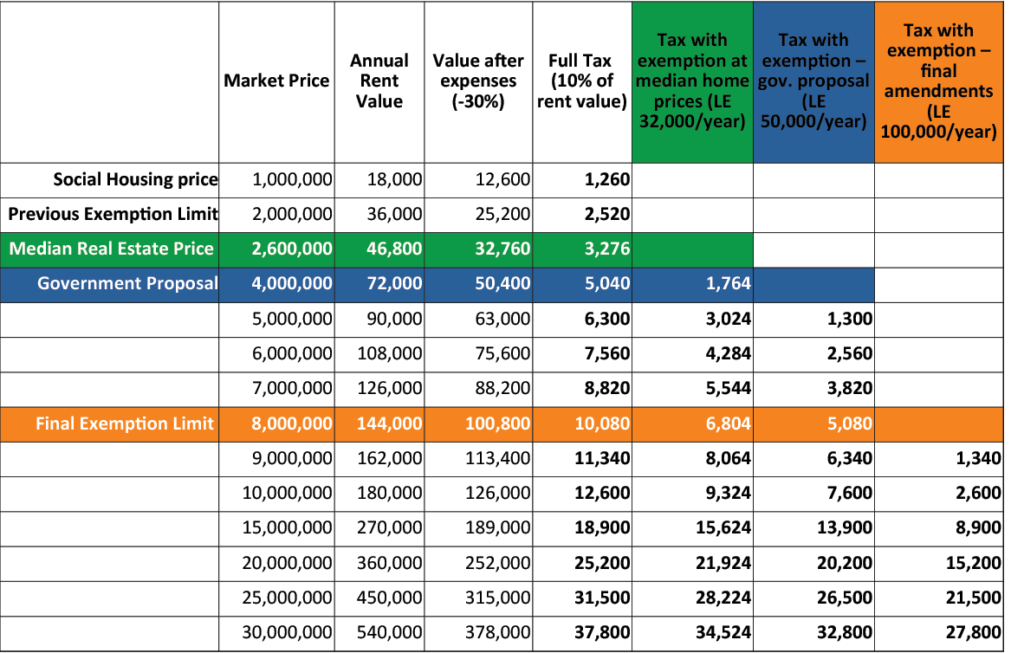

Initially, the government’s draft amendment to Article 18 proposed doubling the exemption ceiling for the primary dwelling from LE 24,000 to LE 50,000 in annual rent (Table 1).2 The Minister of Finance justified this amendment by saying that “It is in line with the philosophy of the law, taking into account the social dimension in light of the effects of inflation and the decline in the purchasing power of money.”3 In other words, the old exemption limit was set in 2014 when the average price of real estate was much lower than it is today, so it is important to increase the exemption limit to keep pace with the increase in average real estate prices.

Table 1: Tax calculations on units according to different exemption limits and without any exemption (pounds)

Senators rejected this amendment, arguing to double it to LE 100,000, with some going so far as to demand full tax exemption for private family homes. The government believed that this would significantly weaken its tax revenues, leaving only 2% of real estate subject to taxation.4 Ultimately, however, the Senate ruled that the proposed exemption threshold was too low given the rate of inflation over the years since the law was passed, the “jumps in the capital and replacement value of real estate… and the market reality of rental value.” They approved an increase in the exemption limit to LE100,000 (a market value of LE8 million per unit), arguing that it represented “a balance between preserving the right to adequate housing and ensuring that the exemption does not spill over into the realm of luxury and excess wealth.”5 This was finally approved by the House of Representatives.

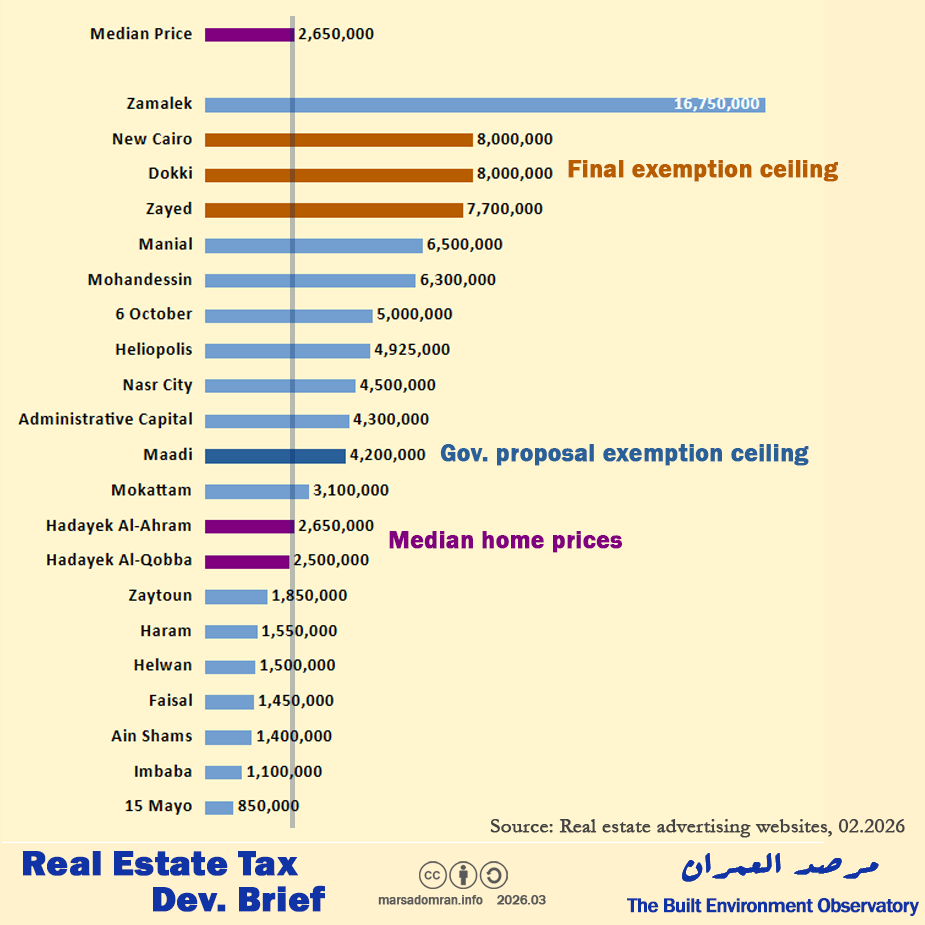

But where is the data on which the Minister of Finance or MPs based their discussion of the fairness of the exemption threshold? In the absence of such data, we relied on real estate search engines. Our analysis showed that the median price of homes in Greater Cairo at the beginning of 2026 was LE 2.6 million, which represents values in the neighborhoods of Hadayek al-Qobba, Hadayek al-Ahram, and Mokattam (Figure 1).6 The median price was chosen rather than the average because it lies in the middle of the data range and is not affected by outliers. These neighborhoods thus represent middle-income communities, while prices below the median represent low-income communities, such as in the neighborhoods of Al-Zaytoun, Faisal, and Helwan. Prices above the median represent upper-middle-income and rich communities, such as Mohandessin, Heliopolis, and Zamalek.

With the signing of the final exemption limit approved by the House of Representatives at LE 8 million (LE100,000 annual rent), we find that it only matches the median prices in the neighbourhoods of New Cairo, Sheikh Zayed, and Dokki, and there is no residential neighbourhood with a higher price among the surveyed neighbourhood except Zamalek (16.7 million pounds). This will exempt the majority of the population from the tax, except for the wealthiest. Compared to the government’s original proposal, which set an exemption limit of 4 million pounds (50,000 pounds annual rent), we find that the government’s proposal is closer to the median price (1.5 times) and corresponds to the Maadi neighbourhood, thus exempting only middle-class and working-class neighbourhoods.

Figure 1: Median cash sale prices of properties for sale in Greater Cairo in February 2026 (LE). Source: Real estate search engines.

2. One-third of properties are subject to tax

The exemption limit applies to one unit used by the household – defined as the spouses and their children up to the age of 18, as its main residence; therefore, any other units owned by the household, whether vacant, used for non-residential purposes, or rented out for residential or non-residential purposes (except for those rented out under the Old Rent Law – Article 4), are subject to tax. According to the 2017 census, there were 23.5 million households living in residential units, representing only 55% of the total 43 million units captured by the census (Figure 2). This means that the remaining 9.6 million non-residential units (22% of the total) and 9.9 million unoccupied residential and non-residential units (representing 23% of the total) are fully subject to Real Estate Tax without exemptions because they are not the owner’s private residence or are used for non-residential activities. However, given the uncertainty surrounding the condition of these properties, it has been estimated that an average of 75% of them could be subject to tax, i.e., 14.6 million units.

Figure 2: Distribution of real estate units by activity. Source: Central Agency for Public Mobilization and Statistics, 2017 Population, Housing, and Buildings Census.

In addition, a portion of the occupied residential units – first homes, are also subject to the tax. There are of course units whose values exceed the exemption limit, but since the exemption limit is high, the Ministry of Finance estimated that they amount to only 2% of such units. Other occupied residential units subject to the Real Estate Tax are some 1.6 million New Rent units, representing 3.7% of total units. These will grow significantly when the Old Rent units, currently tax exempt, are recovered by their owners after the promulgation of the Old Rent Decontrol Law last year. Overall, at least one third of all built property in Egypt is subject to Real Estate Tax.

3. Improving Collection Efficiency

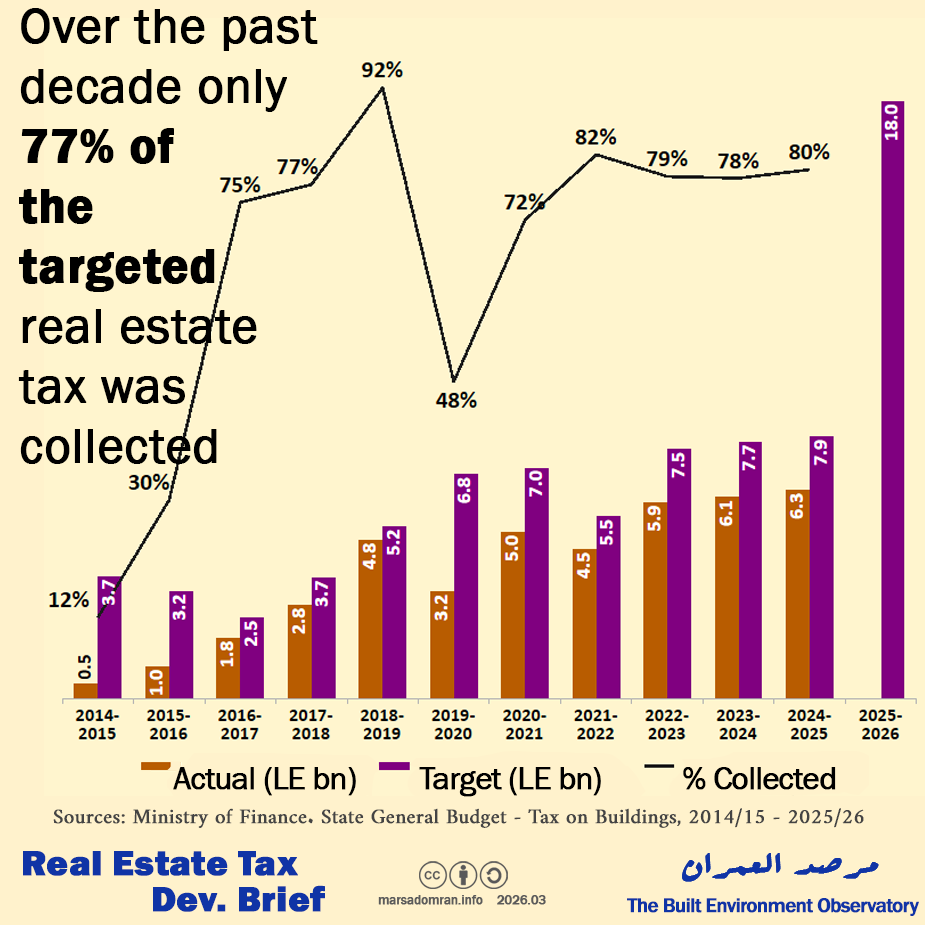

What is the importance of taxes if their collection is low? When analyzing the state general budget data, it was noted that actual tax collection rates were much lower than the targets, averaging 77% of the estimated tax over the past ten years (Figure 3). This may be attributed to a failure to fully inventory real estate units, tax evasion, or lack of collection resources. What is of more concern, are the years in which total tax collection was lower than in the previous year, indicating a decline in collection efficiency as nominal home prices in Egypt rarely fall. This in all likelihood is due to increased tax evasion or a significant lack of capacity to collect in those years.

Figure 3: Targeted and actual real estate tax collection values over the past ten years, 2014/15–2024/25 (LE billion). Source: Ministry of Finance – State General Budget – Tax on Buildings, various years.

In any case, improving the efficiency of tax collection and the fairness of its application will contribute to increasing revenue because taxpayers will feel that it is applied to everyone and not just to some. This is the aim of some of the recent amendments, which include incentives for taxpayers in the form of a 25% discount on the amount due if paid on time (Article 14 bis of the draft). But are these measures sufficient to raise the target revenue for the current fiscal year to LE 18 billion, or about three times the actual revenue?

4. Improving Assessment Transparency

Article 4 of the draft law stipulates that the Real Estate Tax Authority must publish details of the indicative price map 60 days before the start of the (five-year) reassessment, in addition to specifying the assessment bases and criteria in the executive regulations to be issued after the law is published. This is a good step for more than one reason. First, it will become clear to owners the different price levels of neighbouring properties, which supports challenging assessments if they are outside this index. Second, the price map will create some sort of index for real estate prices that unifies all the valuation values needed by other laws, such as reconciliation, betterment levies, Old Rent, etc., in addition to increasing transparency in the real estate market and working towards regulating it.

5. Aspects Skipped by Amendments: Regulating Real Estate Market and Rents

Although the amendments address many aspects of the law, there are other aspects that have not been addressed, chief among them being utilising the real estate tax to regulate the real estate market.

Rental Price Regulation

With rents spiralling out of control in Egypt, the Real Estate Tax could play a pivotal role in regulating rental prices. Two mechanisms can be applied to encourage social rent and help resolve the rental crisis. The first is to exempt New Rent units if they are rented out at fair values set by the government, for example, net rental values calculated by the Real Estate Tax Authority (RTA), which are significantly lower than market values.

The second mechanism is to increase the tax on second homes, holiday homes, and generally vacant units because they are withdrawn from the real estate market and do not benefit society. The increase can be calculated according to the years and reasons for closure up to 50% more than the standard rate. This will contribute to working towards exploiting them, either through rent or sale, which will increase supply in the market, and work to bring down values.

Real Estate Price Regulation

If the real estate tax is imposed on a progressive basis – the tax rate increases as the value of the property increases, the tax will serve to curb inflated property prices and set upper limits. This can lead to encouraging developers to build smaller units that do not have luxury amenities such as golf courses, as well as encouraging homeowners to divide larger properties into smaller ones that can benefit a larger number of residents. It can also slow down the pace of luxury construction, which consumes a larger share of natural resources and facilities.

Improving the Image of the Tax: Redistributing Expenditure

Under the current law, real estate tax revenues go to the Treasury (Ministry of Finance), then 25% of the tax collected within each governorate, is reallocated to those governorates, and another 25% is allocated for the development of informal settlements, leaving 50% of the tax to be allocated by the public treasury as it sees fit.

Therefore, ordinary residents do not see the results of the tax that they paid for in a direct manner, which increases their rejection of the tax. Since the government has announced the end of the unsafe areas (slums) development program, a quarter of the revenues are now free to reallocate. Here, it is proposed that at least 50% of tax revenue is kept at the local level – neighbourhoods and village units, to spend on local urban services such as waste collection, tree planting, road maintenance, lighting, etc… This will contribute to increasing public acceptance of the tax after seeing how it is spent, while local budget deficits of lower-income councils can be balanced by the Treasury’s share.

Abolish Betterment Levies

There is another form of real estate tax imposed on properties adjacent to public urban redevelopment projects such as transport and replanning, known as the betterment levy under Law 222/1955, with the aim of partially financing the costs of these projects. This tax is also considered a wealth tax because it is imposed after the project is implemented and not when the property is sold. It is also calculated at high market prices and not on an imputed basis as real estate taxes are calculated. There is a suspicion of double taxation here, because the real estate tax already takes into account the improvement to the property when it is revalued. Furthermore, the tax on real estate transactions – capital gains tax, which is levied on the property when it is sold at 2.5% of the sale price, directly reflects the increase in value after the improvement, as property prices in the vicinity of the improvements would appreciate. Therefore, in light of the real estate tax amendments, the betterment levy should be abolished.

References and Notes

1 See our legal archive for Law 196/2008 and its amendments.

2 The net assumed value after deducting 30% for expenses and maintenance.

3 Cabinet. “Draft law amending certain provisions of the Real Estate Tax Law 196/2008 – Explanatory Notes.” July 2025.

4“Finance Minister explains: New Real Estate Tax law eases burden on citizens.” Al-Youm Al-Sabea, March 1, 2026.

5 Senate. “Report of the Finance and Investment Committee on the draft law submitted by the government and referred by the House of Representatives amending certain provisions of the Real Estate Tax Law196/2008.” 9 December 2025.

6 While Greater Cairo does not represent the entire Egyptian real estate market, the city has a wide range of neighbourhoods that are sufficient to provide an abstract view of the urban market, excluding rural property values. To establish a more accurate exemption limit, a database of all cities in the country must be created based on real estate transaction tax data (capital gains tax). All data is based on the prices of complete residential units sold in cash on the real estate market in more than 40,000 advertisements on real estate search platforms covering a during a six-month period between August 2025 and February 2026 in the governorates of Cairo and Giza (Greater Cairo). All non-residential properties (commercial/administrative/land) were excluded, as were residential units sold on an installment basis, furnished units, and incomplete units (unfinished/half-finished).